Over the last year and a half, we’ve seen a large volume of transactions involving the acquisition of privately owned BC corporations, especially in the technology sector. In transactions such as these, it’s common for qualifying vendors to try to claim their lifetime capital gains exemption1 (LCGE) against capital gains from the disposition of qualifying small business corporation (QSBC) shares.2 To claim the LCGE, an individual (or a related person) generally needs to have held the shares that are being disposed of for two years, and the corporation in which the shares are held needs to be both a small business corporation (SBC)3 and a Canadian-controlled private corporation (CCPC),4,5 and needs to hold certain Canadian assets over a two-year period.6

The purpose of this article is to illustrate the complexity of the rules at the corporate level—particularly the complexity of the modified test that applies to holding corporations.

SBC test (the SBC 90% test at closing)

At the time of the disposition, the corporation must be an SBC,7 which is defined to include the following requirements:

- It must be a CCPC;8 and

- It must have at least 90% of the fair market value (FMV) of its assets attributable to:9

- Assets that are used principally (more than 50%) in an active business carried on primarily (more than 50%) in Canada (by the corporation or by a related corporation)10—referred to in this article as “50% Canadian operating assets”;

- Shares of the capital stock or indebtedness of one or more SBC that are connected to the particular corporation;11 or

- Assets described in (a) and (b).12

FMV asset test (the 50% over two years test)

In addition to the requirement that it be an SBC at disposition, the corporation being tested for QSBC purposes must also meet certain conditions throughout the 24 months preceding the disposition (meaning at any given point in time during the preceding two years). Specifically, throughout that period, at least 50% of the FMV of its assets must be attributable to:13

- 50% Canadian operating assets;14 or

- Shares or indebtedness of a connected corporation:

The modified FMV asset test (the modified 90% test)

When the sellers are selling shares of a personal holding company, the FMV asset test can be modified. If, throughout the 24 months preceding and including the disposition of holding company shares, at least 90% of the FMV of the assets of the holding company (or a connected corporation) are not attributable to points 1 or 2 of the FMV asset test above, the 50% Canadian operating asset test (bullet 2(b) of the FMV asset test) should be modified to a 90% Canadian operating asset test for any connected corporations.17

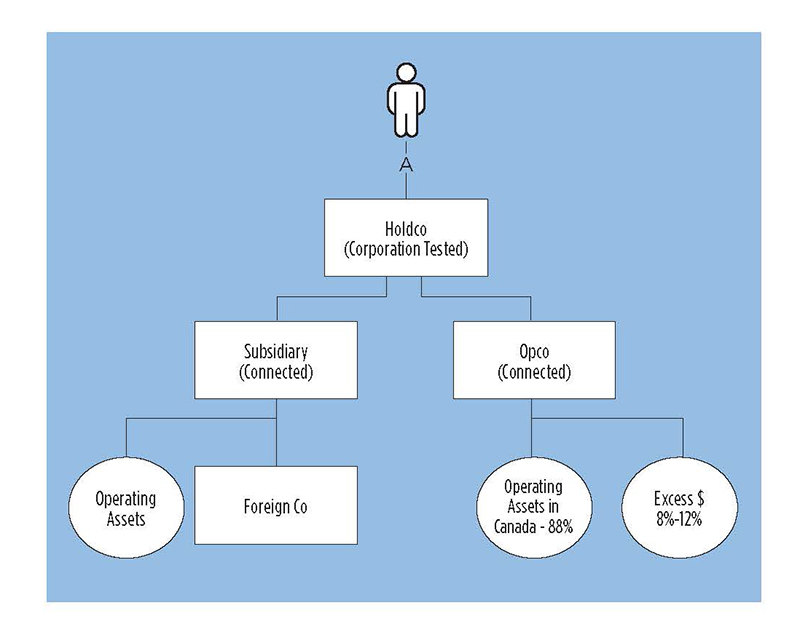

The following illustration provides an example where the opportunity to claim the LCGE on the disposition of “Holdco” shares could be at risk and requires analysis:

In this example, the value of the shares of Holdco is attributable to shares of “Subsidiary” and “Opco.” A number of facts and assumptions are missing—for example, we don’t know the value of the assets or the relative values of Subsidiary and Opco.

Since the value of Subsidiary is 100% attributable to assets other than Canadian operating assets, the shares of Subsidiary do not constitute a good asset for the purposes of the FMV asset test in Holdco. And although it appears that the assets of Opco would meet the base 50% Canadian operating asset test and that only some minor purification may be required to meet the SBC test at closing, the rules require that the modified FMV asset test be considered.

Additionally, if at any point during the preceding two years, Subsidiary represented more than 10% of the FMV of Holdco’s assets, less than 90% of Holdco’s assets (shares of Subsidiary and Opco) would meet the FMV asset test. As a result, the modified FMV asset test would be applied. This means that 50% of the value of Holdco’s assets (per the 50% over two years test) would need to be good assets.18

Given that Subsidiary would fail the test, we can now focus on Opco. We need to ensure that the value of Opco’s assets is at least 90% attributable to Canadian operating assets.

In this example, we know that 8% to 12% of the FMV of Opco’s assets are represented by excess cash. Whether cash is considered to be incidental and pertaining to an active business that is primarily carried out in Canada (and therefore a “good asset”) is a question of fact (see “Other considerations” below).

If at any point in time during the preceding two years, 12% of Opco’s value was attributable to cash that could not be considered a good asset, the modified FMV asset test would not be met and the shares of Holdco would not qualify as QSBC shares. Therefore, the seller would not be able to claim their LCGE.

However, if no more than 10% of that cash was considered a “bad asset,” Opco’s assets would meet the modified FMV asset test. Note that this would not be sufficient to conclude that the shares of Holdco are QSBC shares and that the seller would be able to claim their LCGE. As indicated in the FMV asset test earlier, 50% of the FMV of Holdco’s assets need to be attributable to “good” assets (considering the modified 90% test). Therefore, if the value of Subsidiary’s shares exceeds 50% of the FMV of Holdco’s assets, Holdco would be disqualified from being a QSBC even if Opco meets the modified 90% test. However, if the FMV of Subsidiary’s shares represented no more than 50% of the FMV of Holdco throughout the preceding two years, the modified test would apply. This would not necessarily prevent Holdco’s shares from qualifying as QSBC shares.

Finally, even if Holdco were to meet the FMV asset test (considering the 90% modified test discussed earlier), it would still be required to meet the 90% SBC test at closing.

Clearly, these tests can be daunting and complex—both to read and apply. In practice, it may also be difficult to demonstrate the FMV of each asset at any given point in time in a two-year look-back period. In instances where normal purification techniques (see “Other considerations” below) could be used to meet the SBC requirements before closing, these techniques would not permit purification on a two-year look-back.

Ultimately, the illustrated example does not provide sufficient facts to be able to conclude whether the shares of Holdco are QSBC shares and, therefore, whether the seller would be able to claim their LCGE on the disposition of the Holdco shares.

Other considerations

Valuation

Given the complexity of these tests, it is critical to have an understanding of the valuation of shares, indebtedness, and other assets held by the target corporation. Sellers should carefully discuss these matters with their tax advisors and consider the possibility of obtaining an independent valuation of all relevant assets—particularly as it may be difficult to do a valuation for the past two-year period.

Signing and closing at different times

Although this topic is outside the scope of this article, it’s important to note that signing and closing at different times on the sale of shares to a non-resident or public corporation should not prevent shareholders from applying the LCGE against capital gains incurred as part of the sale transaction. For the purposes of QSBC share testing, the rights to acquire a corporation’s shares pursuant to a share purchase agreement do not have to be considered.19

Purification

As shown in the illustrated example, determining whether assets are good or bad for the purpose of QSBC share testing is not always a straightforward exercise. Sellers should consult their tax advisors to determine if a purification strategy is needed.20 Note that purchasers may also be interested in considering purification steps and the associated risks from a tax due diligence perspective.

For example, sellers must consider if cash is excess or incidental and if it pertains to the active business otherwise carried out by a target corporation. The Canada Revenue Agency21 and the courts22 have provided commentary that can assist sellers in assessing whether or not purification is required.

As previously mentioned, in circumstances where a target corporation’s shares are held via a personal holding company, it may be impossible to undertake any purification transactions.

Closing thoughts

As described in this article, LCGE rules are complex. Taxpayers should consider isolating bad assets, such as marketable securities or foreign assets, in a separate holding corporation and managing excess cash. Moreover, because a transaction is not always foreseeable when implementing a holding company structure, taxpayers should consult with their advisors when considering holding the shares of an operating CCPC in a holding corporation or in a chain of holding corporations.

Author

Justine Alder, CPA, is a senior manager at PwC Canada, based in Vancouver. She specializes in corporate tax, with a focus on strategy, co-ordination, reporting, and process automation for entrepreneurial organizations, primarily in knowledge-based industries, that are expanding in Canada and globally. She thanks Caroline Morin, M.Fisc., member of the law societies of Quebec and British Columbia, and other PwC colleagues for their contributions to this article.

This article was originally published in the November/December 2022 issue of CPABC in Focus.

Footnotes

1 The lifetime limit is $913,630 (for 2022, indexed annually).

2 Subsection 110.6(1) of Canada’s Income Tax Act (ITA).

3 Subsection 248(1) of the ITA.

4 Subsection 125(7) of the ITA.

5 Note that a series of changes with respect to substantive CCPC was announced in the 2022 federal budget. The analysis and implications of these rules is beyond the scope of this article. Taxpayers are encouraged to consult with their advisors to assess the implications of these rules for particular transactions.

6 QSBC shares are defined in subsection 110.6(1) of the ITA.

7 Paragraph (a) of the definition of QSBC shares in subsection 110.6(1) of the ITA.

8 Subsection 248(1) of the ITA.

9 Preamble of the definition of SBC in subsection 248(1) of the ITA.

10 Paragraph (a) of the definition of SBC in subsection 248(1) of the ITA.

11 Paragraph (b) of the definition of SBC in subsection 248(1) of the ITA.

12 Paragraph (c) of the definition of SBC in subsection 248(1) of the ITA.

13 Preamble of paragraph (c) of the definition of QSBC shares in subsection 110.6(1).

14 Subparagraph (c)(i) of the definition of QSBC shares in subsection 110.6(1) of the ITA.

15 Clause A of subparagraph (c)(i) of the definition of QSBC shares in subsection 110.6(1) of the ITA.

16 Paragraph (c)(ii) of the definition of QSBC shares in subsection 110.6(1) of the ITA.

17 Paragraph (d) of the definition of QSBC shares in subsection 110.6(1) of the ITA. Note that one must not confuse which of the 50% tests is modified, as paragraph (c) of the definition of QSBC shares in subsection 110.6(1) of the ITA includes more than one 50% test: one in the preamble that does not get modified and one in clause B that gets modified for connected corporations.

18 The modified 90% test modifies the testing inside the connected corporations of Holdco, meaning the assets of Subsidiary and Opco. Note that this example is very simplified and does not illustrate what could happen in a chain of holding corporations. Prudence is required when reading the rules.

19 Paragraph 110.6(14)(b) of the ITA. As indicated in footnote 5, taxpayers should consult with their tax advisors to consider whether the substantive CCPC rules could otherwise apply and affect their planning for the disposition of shares in any manner whatsoever.

20 A detailed review of purification strategies is beyond the scope of this article. There are numerous papers and articles on this topic that can be accessed online, including: John Oakey, “Company Purification—Don’t Take the Short-Cut,” All About Estates (blog), June 22, 2021.

21 CRA document no. 2009-0330071C6F.

22 For example, see Skidmore v. R., [2000] 2 C.T.C. 325 (FCA) and R. v. Ensite Ltd., [1986] 2 C.T.C. 459 at paragraphs 14 and 15.

")